S&P500 Trading Update 14/5/26

S&P500 Trading Update 14/5/26

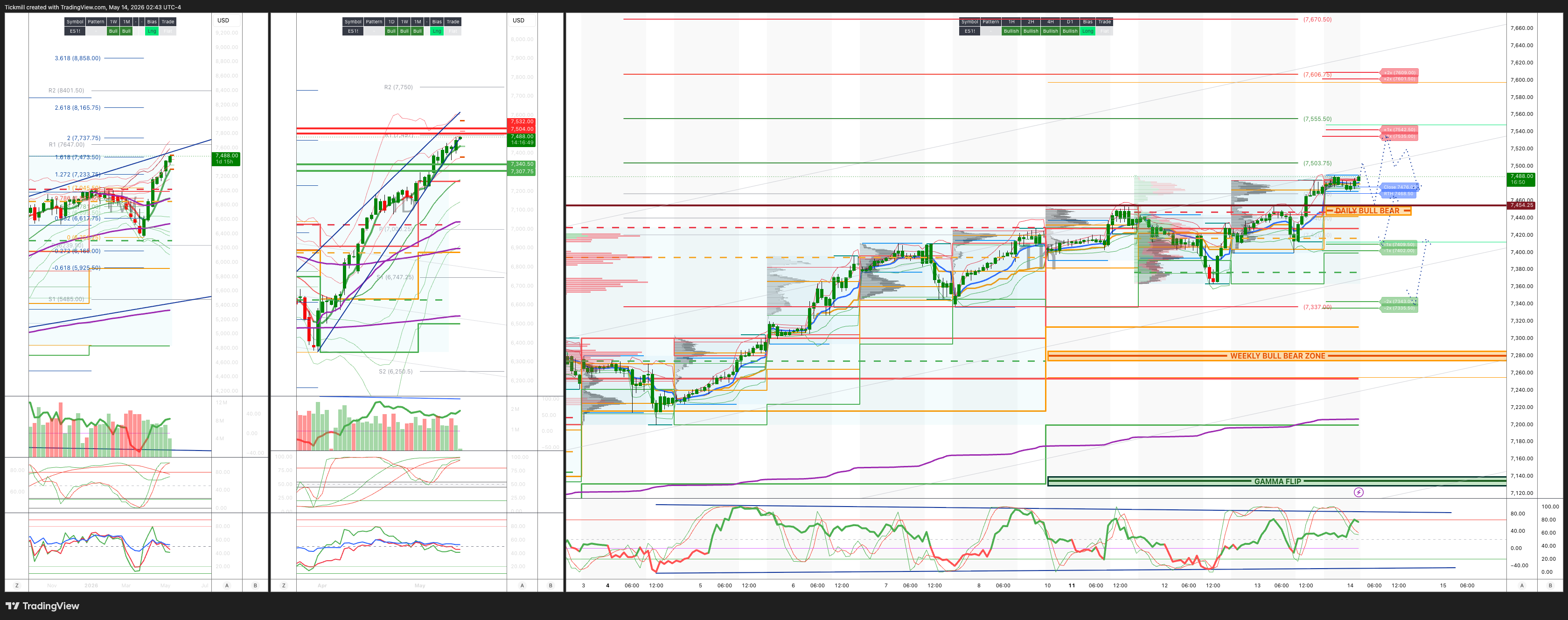

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7280/70

WEEKLY RANGE RES 7504/32 SUP 7340

May OPEX Straddle: 225pt range implies a OPEX to OPEX range of [6900, 7350]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.2 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7445

WEEKLY VWAP BULLISH 7255

MONTHLY VWAP BULLISH 6898

DAILY STRUCTURE – OTFH - 7399

WEEKLY STRUCTURE – OTFH - 7199

MONTHLY STRUCTURE - OTFH - 6514

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Down (OTFD): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7445/55

GAMMA FLIP 7135

DELTA FLIP 6932

DAILY RANGE RES 7535 SUP 7402

2 SIGMA RES 7601 SUP 7335

VIX BULL BEAR ZONE 19.47

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET DAILY/WEEKLY RANGE RES

SHORT ON REJECT/RECLAIM DAILY/WEEKLY RANGE RES TARGET DAILY BULL BEAR ZONE

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Rates & Semis’

US Close: Indices Higher, Breadth Weak, Rates Still the Macro Ceiling

US equities closed higher, led by tech, but the tape was narrow and increasingly dependent on a small group of mega-cap winners. S&P +58bps to 7,444, NDX +104bps to 29,367, R2K +4bps to 2,844, while the Dow slipped -14bps to 49,693. Volumes were in line with average at 19bn shares, and the MOC was a sizable USD 4.4bn to sell.

Cross-asset moves were mixed: VIX -28bps to 17.94, WTI -78bps to USD 101.28, 10Y +1bp to 4.47%, gold -58bps to USD 4,688, DXY +21bps to 98.50, and Bitcoin -130bps to USD 79,622.

Main message

The market continues to grind higher despite a difficult macro backdrop: hotter inflation, higher yields, hawkish Fed rhetoric, geopolitical risk, and oil still above USD 100. But the quality of the move is deteriorating. Around 65% of S&P 500 stocks closed lower, even as the index rose, and five companies — NVDA, AAPL, GOOGL, AMZN, and AVGO — have accounted for roughly 50% of S&P 500 growth since April 1st.

This remains a market where mega-cap AI and tech leadership can carry the indices, but breadth and consumer weakness are flashing caution.

Inflation and rates: PPI keeps pressure on the Fed path

The April PPI print came in hotter than expected, following a firmer-than-expected CPI print the day before. Based on both reports, the desk estimates core PCE +0.30% m/m in April, with the year-over-year rate at +3.32%.

That matters because the market is already worried about energy passthrough and sticky services inflation. With oil still above USD 100, inflation relief is not coming quickly enough to give the Fed much room.

Rates remained the central macro focus. The 10Y and 30Y both retested local highs, with the 10Y reaching its highest level since July and the 30Y its highest intraday level since last May. The drivers were straightforward: hawkish Fed rhetoric, geopolitical worries, and hotter inflation data.

The equity market is still absorbing higher yields, but the risk is that duration-sensitive parts of the market eventually start to break if yields continue higher.

Tech: still leading, but increasingly narrow

The standout feature of the session was continued tech outperformance despite higher yields. The desk remains focused on the strength in non-profitable tech, which is unusual in a rising-rate environment.

The immediate catalyst was positioning ahead of the Trump/Xi meeting, with Jensen Huang joining the trip last minute alongside other business leaders. That helped support AI-related names, with NVDA / SMH +2%.

But the leadership is narrow. Tech is carrying the market, and within tech, a small handful of mega-cap AI/platform names are doing most of the work. That is not necessarily bearish in the short term, but it increases fragility. If these leaders pause, the index has less support underneath.

Breadth: headline strength, weak participation

The S&P closed higher, but roughly 65% of S&P stocks were down on the session. This is the core tension in the market: indices are making new all-time highs, but participation is weak.

This kind of tape can persist for a while, especially when the largest index weights have strong earnings, AI narratives, and global sponsorship. But it also means the market is vulnerable to a reversal in leadership. A narrow rally can look stable until the top names stop working.

The breadth message is simple: the index is strong, but the average stock is not.

Consumer discretionary: still the weak link

Consumer discretionary underperformed again, with momentum longs down around 1%. Top-down consumer sentiment remains very bearish. The concern is no longer just about weak companies; even good consumer stories are now being questioned, particularly if they trade at high multiples.

The pressure points remain:

Higher gasoline prices

Hotter inflation

Higher financing costs

Weak lower-income consumer read-throughs

Rotation into AI/tech

Skepticism around forward guidance and margins

WMT next week is important for this theme. The market will watch closely for evidence of trade-down, food inflation pressure, discretionary weakness, and whether the low-end consumer is worsening or stabilizing.

Flows: better to buy, but split by investor type

Floor activity was moderate at 4/10, but flows were constructive, finishing +5.5% better to buy versus a 30-day average of +192bps.

Asset managers were USD 1.5bn better to buy, led by info tech, industrials, and financials, while selling consumer discretionary. Hedge funds were USD 2bn net buyers, led by communication services and consumer discretionary, while selling info tech and industrials.

The interesting point is that hedge funds bought some consumer discretionary even as the group underperformed, suggesting some tactical dip-buying or short-covering may be emerging. But asset managers continue to sell the group, which keeps the broader sponsorship weak.

Derivatives: spot-up / vol-up regime remains the key feature

The vol desk remains focused on the persistent spot-up / vol-up dynamic and the skew crush in both NDX and SPX. NDX vol remains very high versus SPX, making tech hedges expensive and pushing more hedging flow into SPX.

A striking point: NDX spot and vol have moved in tandem for six consecutive sessions, the longest streak on record. That is not normal bull-market behavior. It means investors are buying upside or maintaining exposure while also paying for protection around event risk.

The desk likes outright puts here because skew is flat, making downside protection more attractive. They also like upside in single names in the ADR space. With attention turning to the Trump/Xi meeting, the straddle for the rest of the week went out around 85bps.

Trading takeaways

Stay long the AI/mega-cap leadership, but recognize that the trade is increasingly crowded and narrow. The index can keep grinding higher if NVDA, AAPL, GOOGL, AMZN, and AVGO keep working, but weak breadth raises the risk of a sharper pullback if leadership cracks.

Avoid chasing non-profitable tech aggressively with yields at local highs. The strength is notable, but it is also increasingly vulnerable if rates continue to rise.

Consumer discretionary remains a funding source. Tactical bounces are possible given bearish sentiment, but the top-down backdrop is still poor. WMT next week is the key catalyst.

Use SPX options for hedging if NDX vol remains too rich. With skew flat, outright puts look more attractive than usual.

Watch the Trump/Xi meeting closely. A constructive outcome could extend the AI/tech leadership trade, while disappointment could pressure crowded winners and reinforce the need for hedges.

The headline tape was bullish, but the internals were not. The S&P and Nasdaq rose, yet most stocks fell, rates stayed near local highs, inflation data remained sticky, and consumer discretionary continued to weaken. This is still an AI-led market, and the leadership remains powerful, but the rally is becoming narrower and more dependent on a handful of names.

For now, the right stance is constructive but more disciplined: stay with the winners, avoid chasing weaker breadth, keep hedges on, and treat consumer discretionary with caution until inflation, oil, or guidance improves.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!